Need a business plan? Call now:

Talk to our experts:

- Business Plan for Investors

- Bank/SBA Business Plan

- Operational/Strategic Planning

- L1 Visa Business Plan

- E1 Treaty Trader Visa Business Plan

- E2 Treaty Investor Visa Business Plan

- EB1 Business Plan

- EB2 Visa Business Plan

- EB5 Business Plan

- Innovator Founder Visa Business Plan

- UK Start-Up Visa Business Plan

- UK Expansion Worker Visa Business Plan

- Manitoba MPNP Visa Business Plan

- Start-Up Visa Business Plan

- Nova Scotia NSNP Visa Business Plan

- British Columbia BC PNP Visa Business Plan

- Self-Employed Visa Business Plan

- OINP Entrepreneur Stream Business Plan

- LMIA Owner Operator Business Plan

- ICT Work Permit Business Plan

- LMIA Mobility Program – C11 Entrepreneur Business Plan

- USMCA (ex-NAFTA) Business Plan

- Franchise Business Planning

- Landlord Business Plan

- Nonprofit Start-Up Business Plan

- USDA Business Plan

- Cannabis business plan

- eCommerce business plan

- Online Boutique Business Plan

- Daycare business plan

- Mobile Application Business Plan

- Restaurant business plan

- Food Delivery Business Plan

- Real Estate Business Plan

- Business Continuity Plan

- Buy Side Due Diligence Services

- ICO whitepaper

- ICO consulting services

- Confidential Information Memorandum

- Private Placement Memorandum

- Feasibility study

- Fractional CFO

- How it works

- Business Plan Templates

Goals and Objectives for Business Plan with Examples

Published Nov.05, 2023

Updated Apr.23, 2024

By: Jakub Babkins

Average rating 5 / 5. Vote count: 2

No votes so far! Be the first to rate this post.

Table of Content

Every business needs a clear vision of what it wants to achieve and how it plans to get there. A business plan is a document that outlines the goals and objectives of a business, as well as the strategies and actions to achieve them. A well-written business plan from business plan specialists can help a business attract investors, secure funding, and guide its growth.

Understanding Business Objectives

Business objectives are S pecific, M easurable, A chievable, R elevant, and T ime-bound (SMART) statements that describe what a business wants to accomplish in a given period. They are derived from the overall vision and mission of the business, and they support its strategic direction.

Business plan objectives can be categorized into different types, depending on their purpose and scope. Some common types of business objectives are:

- Financial objectives

- Operational objectives

- Marketing objectives

- Social objectives

For example, a sample of business goals and objectives for a business plan for a bakery could be:

- To increase its annual revenue by 20% in the next year.

- To reduce its production costs by 10% in the next six months.

- To launch a new product line of gluten-free cakes in the next quarter.

- To improve its customer satisfaction rating by 15% in the next month.

The Significance of Business Objectives

Business objectives are important for several reasons. They help to:

- Clarify and direct the company and stakeholders

- Align the company’s efforts and resources to a common goal

- Motivate and inspire employees to perform better

- Measure and evaluate the company’s progress and performance

- Communicate the company’s value and advantage to customers and the market

For example, by setting a revenue objective, a bakery can focus on increasing its sales and marketing efforts, monitor its sales data and customer feedback, motivate its staff to deliver quality products and service, communicate its unique selling points and benefits to its customers, and adjust its pricing and product mix according to market demand.

Advantages of Outlining Business Objectives

Outlining business objectives is a crucial step in creating a business plan. It serves as a roadmap for the company’s growth and development. Outlining business objectives has several advantages, such as:

- Clarifies the company’s vision, direction, scope, and boundaries

- Break down the company’s goals into smaller tasks and milestones

- Assigns roles and responsibilities and delegates tasks

- Establishes standards and criteria for success and performance

- Anticipates risks and challenges and devises contingency plans

For example, by outlining its business objective for increasing the average revenue per customer in its business plan, a bakery can:

- Attract investors with its viable business plan for investors

- Secure funding from banks or others with its realistic financial plan

- Partner with businesses or organizations that complement or enhance its products or services

- Choose the best marketing, pricing, product, staff, location, etc. for its target market and customers

Setting Goals and Objectives for a Business Plan

Setting goals and objectives for a business plan is not a one-time task. It requires careful planning, research, analysis, and evaluation. To set effective goals and objectives for a business plan, one should follow some best practices, such as:

OPTION 1: Use the SMART framework. A SMART goal or objective is clear, quantifiable, realistic, aligned with the company’s mission and vision, and has a deadline. SMART stands for:

- Specific – The goal or objective should be clear, concise, and well-defined.

- Measurable – The goal or objective should be quantifiable or verifiable.

- Achievable – The goal or objective should be realistic and attainable.

- Relevant – The goal or objective should be aligned with the company’s vision, mission, and values.

- Time-bound – The goal or objective should have a deadline or timeframe.

For example, using the SMART criteria, a bakery can refine its business objective for increasing the average revenue per customer as follows:

- Specific – Increase revenue with new products and services from $5 to $5.50.

- Measurable – Track customer revenue monthly with sales reports.

- Achievable – Research the market, develop new products and services, and train staff to upsell and cross-sell.

- Relevant – Improve customer satisfaction and loyalty, profitability and cash flow, and market competitiveness.

- Time-bound – Achieve this objective in six months, from January 1st to June 30th.

OPTION 2: Use the OKR framework. OKR stands for O bjectives and K ey R esults. An OKR is a goal-setting technique that links the company’s objectives with measurable outcomes. An objective is a qualitative statement of what the company wants to achieve. A key result is a quantitative metric that shows how the objective will be achieved.

OPTION 3: Use the SWOT analysis. SWOT stands for S trengths, W eaknesses, O pportunities, and T hreats. A SWOT analysis is a strategic tool that helps the company assess the internal and external factors that affect its goals and objectives.

- Strengths – Internal factors that give the company an advantage over others.

- Weaknesses – Internal factors that limit the company’s performance or growth.

- Opportunities – External factors that allow the company to improve or expand.

- Threats – External factors that pose a risk or challenge to the company.

For example, using these frameworks, a bakery might set the following goals and objectives for its SBA business plan :

Objective – To launch a new product line of gluten-free cakes in the next quarter.

Key Results:

- Research gluten-free cake market demand and preferences by month-end.

- Create and test 10 gluten-free cake recipes by next month-end.

- Make and sell 100 gluten-free cakes weekly online or in-store by quarter-end.

SWOT Analysis:

- Expertise and experience in baking and cake decorating.

- Loyal and satisfied customer base.

- Strong online presence and reputation.

Weaknesses:

- Limited production capacity and equipment.

- High production costs and low-profit margins.

- Lack of knowledge and skills in gluten-free baking.

Opportunities:

- Growing demand and awareness for gluten-free products.

- Competitive advantage and differentiation in the market.

- Potential partnerships and collaborations with health-conscious customers and organizations.

- Increasing competition from other bakeries and gluten-free brands.

- Changing customer tastes and preferences.

- Regulatory and legal issues related to gluten-free labeling and certification.

Examples of Business Goals and Objectives

To illustrate how to write business goals and objectives for a business plan, let’s use a hypothetical example of a bakery business called Sweet Treats. Sweet Treats is a small bakery specializing in custom-made cakes, cupcakes, cookies, and other baked goods for various occasions.

Here are some examples of possible startup business goals and objectives for Sweet Treats:

Earning and Preserving Profitability

Profitability is the ability of a company to generate more revenue than expenses. It indicates the financial health and performance of the company. Profitability is essential for a business to sustain its operations, grow its market share, and reward its stakeholders.

Some possible objectives for earning and preserving profitability for Sweet Treats are:

- To increase the gross profit margin by 5% in the next quarter by reducing the cost of goods sold

- To achieve a net income of $100,000 in the current fiscal year by increasing sales and reducing overhead costs

Ensuring Consistent Cash Flow

Cash flow is the amount of money that flows in and out of a company. A company needs to have enough cash to cover its operating expenses, pay its debts, invest in its growth, and reward its shareholders.

Some possible objectives for ensuring consistent cash flow for Sweet Treats are:

- Increase monthly operating cash inflow by 15% by the end of the year by improving the efficiency and productivity of the business processes

- Increase the cash flow from investing activities by selling or disposing of non-performing or obsolete assets

Creating and Maintaining Efficiency

Efficiency is the ratio of output to input. It measures how well a company uses its resources to produce its products or services. Efficiency can help a business improve its quality, productivity, customer satisfaction, and profitability.

Some possible objectives for creating and maintaining efficiency for Sweet Treats are:

- To reduce the production time by 10% in the next month by implementing lean manufacturing techniques

- To increase the customer service response rate by 20% in the next week by using chatbots or automated systems

Winning and Keeping Clients

Clients are the people or organizations that buy or use the products or services of a company. They are the source of revenue and growth for a company. Therefore, winning and keeping clients is vital to generating steady revenue, increasing customer loyalty, and enhancing word-of-mouth marketing.

Some possible objectives for winning and keeping clients for Sweet Treats are:

- To acquire 100 new clients in the next quarter by launching a referral program or a promotional campaign

- To retain 90% of existing clients in the current year by offering loyalty rewards or satisfaction guarantees

Building a Recognizable Brand

A brand is the name, logo, design, or other features distinguishing a company from its competitors. It represents the identity, reputation, and value proposition of a company. Building a recognizable brand is crucial for attracting and retaining clients and creating a loyal fan base.

Some possible objectives for building a recognizable brand for Sweet Treats are:

- To increase brand awareness by 50% in the next six months by creating and distributing engaging content on social media platforms

- To improve brand image by 30% in the next year by participating in social causes or sponsoring events that align with the company’s values

Expanding and Nurturing an Audience with Marketing

An audience is a group of people interested in or following a company’s products or services. They can be potential or existing clients, fans, influencers, or partners. Expanding and nurturing an audience with marketing is essential for increasing a company’s visibility, reach, and engagement.

Some possible objectives for expanding and nurturing an audience with marketing for Sweet Treats are:

- To grow the email list by 1,000 subscribers in the next month by offering a free ebook or a webinar

- To nurture leads by sending them relevant and valuable information through email newsletters or blog posts

Strategizing for Expansion

Expansion is the process of increasing a company’s size, scope, or scale. It can involve entering new markets, launching new products or services, opening new locations, or forming new alliances. Strategizing for expansion is important for diversifying revenue streams, reaching new audiences, and gaining competitive advantages.

Some possible objectives for strategizing for expansion for Sweet Treats are:

- To launch a new product or service line by developing and testing prototypes

- To open a new branch or franchise by securing funding and hiring staff

Template for Business Objectives

A template for writing business objectives is a format or structure that can be used as a guide or reference for creating your objectives. A template for writing business objectives can help you to ensure that your objectives are SMART, clear, concise, and consistent.

To use this template, fill in the blanks with your information. Here is an example of how you can use this template:

Example of Business Objectives

Our business is a _____________ (type of business) that provides _____________ (products or services) to _____________ (target market). Our vision is to _____________ (vision statement) and our mission is to _____________ (mission statement).

Our long-term business goals and objectives for the next _____________ (time period) are:

S pecific: We want to _____________ (specific goal) by _____________ (specific action).

M easurable: We will measure our progress by _____________ (quantifiable indicator).

A chievable: We have _____________ (resources, capabilities, constraints) that will enable us to achieve this goal.

R elevant: This goal supports our vision and mission by _____________ (benefit or impact).

T ime-bound: We will complete this goal by _____________ (deadline).

Repeat this process for each goal and objective for your business plan.

How to Monitor Your Business Objectives?

After setting goals and objectives for your business plan, you should check them regularly to see if you are achieving them. Monitoring your business objectives can help you to:

- Track your progress and performance

- Identify and overcome any challenges

- Adjust your actions and strategies as needed

Some of the tools and methods that you can use to monitor your business objectives are:

- Dashboards – Show key data and metrics for your objectives with tools like Google Data Studio, Databox, or DashThis.

- Reports – Get detailed information and analysis for your objectives with tools like Google Analytics, Google Search Console, or SEMrush.

- Feedback – Learn from your customers and their needs and expectations with tools like SurveyMonkey, Typeform, or Google Forms.

Strategies for Realizing Business Objectives

To achieve your business objectives, you need more than setting and monitoring them. You need strategies and actions that support them. Strategies are the general methods to reach your objectives. Actions are the specific steps to implement your strategies.

Different objectives require different strategies and actions. Some common types are:

- Marketing strategies

- Operational strategies

- Financial strategies

- Human resource strategies

- Growth strategies

To implement effective strategies and actions, consider these factors:

- Alignment – They should match your vision, mission, values, goals, and objectives

- Feasibility – They should be possible with your capabilities, resources, and constraints

- Suitability – They should fit the context and needs of your business

How OGSCapital Can Help You Achieve Your Business Objectives?

We at OGSCapital can help you with your business plan and related documents. We have over 15 years of experience writing high-quality business plans for various industries and regions. We have a team of business plan experts who can assist you with market research, financial analysis, strategy formulation, and presentation design. We can customize your business plan to suit your needs and objectives, whether you need funding, launching, expanding, or entering a new market. We can also help you with pitch decks, executive summaries, feasibility studies, and grant proposals. Contact us today for a free quote and start working on your business plan.

Frequently Asked Questions

What are the goals and objectives in business.

Goals and objectives in a business plan are the desired outcomes that a company works toward. To describe company goals and objectives for a business plan, start with your mission statement and then identify your strategic and operational objectives. To write company objectives, you must brainstorm, organize, prioritize, assign, track, and review them using the SMART framework and KPIs.

What are the examples of goals and objectives in a business plan?

Examples of goals and objectives in a business plan are: Goal: To increase revenue by 10% each year for the next five years. Objective: To launch a new product line and create a marketing campaign to reach new customers.

What are the 4 main objectives of a business?

The 4 main objectives of a business are economic, social, human, and organic. Economic objectives deal with financial performance, social objectives deal with social responsibility, human objectives deal with employee welfare, and organic objectives deal with business growth and development.

What are goals and objectives examples?

Setting goals and objectives for a business plan describes what a business or a team wants to achieve and how they will do it. For example: Goal: To provide excellent customer service. Objective: To increase customer satisfaction scores by 20% by the end of the quarter.

At OGSCapital, our business planning services offer expert guidance and support to create a realistic and actionable plan that aligns with your vision and mission. Get in touch to discuss further!

OGSCapital’s team has assisted thousands of entrepreneurs with top-rate business plan development, consultancy and analysis. They’ve helped thousands of SME owners secure more than $1.5 billion in funding, and they can do the same for you.

Bowling Alley Business Plan Sample

Nightclub Business Plan (2024): A Comprehensive Guide

Rabbit Farming Business Plan

Beverages Business Plan

Private Schools Business Plan

Business Plan for a Lounge

Any questions? Get in Touch!

We have been mentioned in the press:

Leave a Reply Cancel reply

Your email address will not be published. Required fields are marked *

Save my name, email, and website in this browser for the next time I comment.

Search the site:

Business growth

Business tips

Business objectives: How to set them (with 5 examples and a template)

As anyone who played rec league sports in the '90s might remember, being on a team for some reason required you to sell knockoff candy bars to raise funds. Every season, my biggest customer was always me. Some kids went door-to-door, some set up outside local businesses, some sent boxes to their parents' jobs—I just used my allowance to buy a few for myself.

Aside from initiative, what my approach lacked was a plan, a goal, and accountability. A lot to ask of an unmotivated nine-year-old, I know, but 100% required for anyone who runs an actual business.

Business objectives help companies avoid my pitfalls by laying the groundwork for all the above so they can pursue achievable growth.

Table of contents:

What are business objectives?

What you want the company to achieve

How you can measure success

Which players are involved in driving success

The timelines needed to plan, initiate, and implement steps

How, if successful, these actions can be integrated sustainably going forward

Business objectives vs. goals

Here's what that breakdown could have looked like for nine-year-old me selling candy for my little league team:

Business objective: I will increase my sales output by learning and implementing point-of-sale conversion frameworks. I'll measure success by comparing week-over-week sales growth to median sales across players on my baseball team.

Business goal: I will sell more candy bars than anyone on my team and earn the grand prize: a team party at Pizza Hut.

The benefits of setting business objectives

You might think it's good enough to continue working status quo toward your goals, but as the cliche goes, good enough usually isn't. Establishing and following defined, actionable steps through business objectives can:

Help establish clear roadmaps: You can translate your objectives into time-sensitive sequences to chart your path toward growth.

Set groundwork for culture: Clear objectives should reflect the culture you envision, and, in turn, they should help guide your team to foster it.

Influence talent acquisition: Once you know your objectives, you can use them to find the people with the specific skills and experiences needed to actualize them.

Encourage teamwork: People work together better when they know what they're working toward.

Establish accountability: By measuring progress, you can see where errors and inefficiencies come from.

Drive productivity: The endgame of an objective is to make individual team members and processes more effective.

How to set business objectives

Setting business objectives takes a thoughtful, top-to-bottom approach. At every level of your business—whether you're a massive candy corporation or one kid selling chocolate almond bars door-to-door—there are improvements to make, steps to take, and players with stakes (or in my case, bats) in the game.

1. Establish clear goals

You can't hit a home run without a fence, and you can't reach a goal without setting it. Before you start brainstorming your objectives, you need to know what your objectives will help you work toward.

Increase total revenue by 25% over the next two years

Reduce production costs by 10% by the end of the year

Provide health insurance for employees by next fiscal year

Grow design department to 10+ employees this year

Reach 100k Instagram followers ahead of new product launch

Implement full rebrand before new partnership announcement

Once you have these goals in place, you can establish individual objectives that position your company to reach them.

2. Set a baseline

Like a field manager before a game, you've got to set your baselines. (Very niche pun, I know.) With a definite goal in mind, the only way to know your progress is to know where you're starting from.

Analyzing your baselines could also help you recalibrate your goals. You may have decided abstractly that you want conversion rates to double in six months, but is that really possible? If your measurables show there's potentially a heavier lift involved than you expected, you can always roll back the goal performance or expand the timeline.

3. Involve players at all levels in the conversation

Too often, the most important people are left out of conversations about goals and objectives. The more levels of complexity and oversight, the more important it is to hear from everyone—yet the more likely it is that some will be excluded.

Let's say you want to reduce overhead by 5% over the next two years for your sporting goods manufacturing outfit. At a high level, your team finds you can reduce production costs by using cheaper materials for baseball gloves. A member of your sales team points out that the reduction in quality, which your brand is famous for, could lead to losses that offset those savings. Meanwhile, a factory representative points out that replacing outdated machines would be expensive initially but would increase efficiency, reduce defects, and cut maintenance costs, breaking even in four years.

By involving various teams at multiple levels, you find it's worth it to extend timelines from two to four years. Your overhead reduction may be lower than 5% by year two but should be much higher than that by year four based on these changes.

The takeaway from this pretty crude example is that it's helpful to make sure every team that touches anything related to your objective gets consulted. They should give valuable, practical input thanks to their boots- (or cleats-) on-the-ground experience.

4. Define measurable outcomes

An objective should be exactly that. Using KPIs (key performance indicators) to apply a level of objectivity to your action steps allows you to measure their progress and success over time and either adapt as you go along or stay the course.

How do you know if your specific objectives are leading to increased web traffic, or if that's just natural (or even incidental) growth? How do you know if your recruiting efforts lead to better candidates, or whether your employees are actually more satisfied? Here are a few examples of measurable outcomes to show proof:

Percentage change (15% overall increase in revenue)

Goal number (10,000 subscribers)

Success range (five to 10 new clients)

Clear change (new company name)

Executable action (weekly newsletter launch)

5. Outline a roadmap with a schedule

You've got your organizational goals defined, logged your baselines, sourced objectives from across your company, and know your metrics for defining success. Now it's time to set an actionable plan you can execute.

Your objectives roadmap should include all involved team members and departments and clear timelines for reaching milestones. Within your objectives, set action items with deadlines to stay on track, along with corresponding progress markers. For the objective of "increase lead conversion efficiency by 10%," that could look like:

May 15: Begin time logging

June 1: Register team members for productivity seminar

June 15: Integrate Trello for managing processes

June 15: Audit time log

August 1: Audit time log—goal efficiency increase of 5%

6. Integrate successful changes

You've successfully achieved your objectives—great! But as Yogi Berra famously said, "It ain't over till it's over," and it ain't over yet.

Don't let this win be a one-off accomplishment. Berra also said "You can observe a lot by just watching," and applying what you observed from this process will help you continue growing your company. Take what worked, and integrate it into your business processes for sustainable improvement. Then create new objectives, so you can continue the cycle.

Examples of business objectives and goals

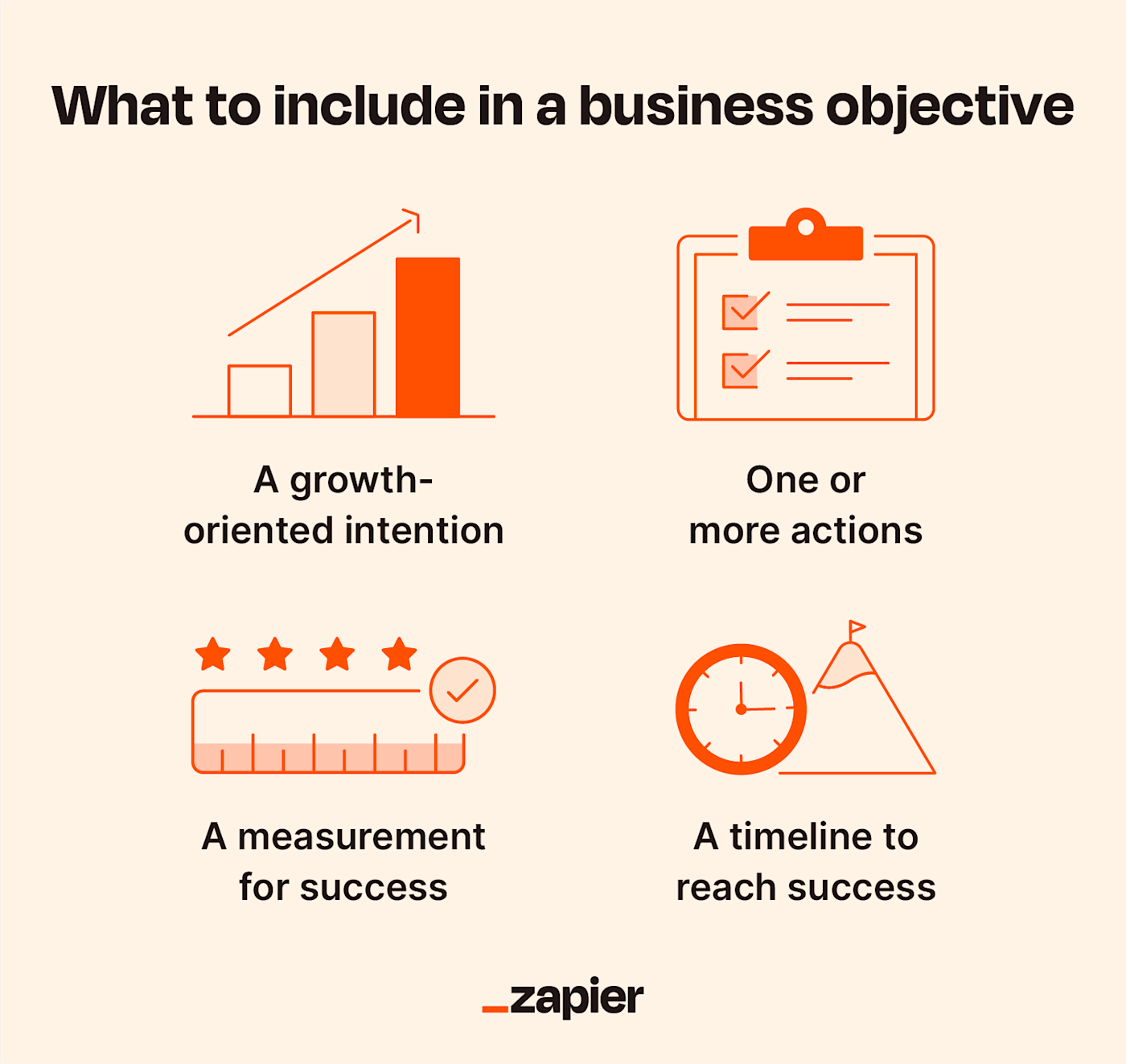

Business objectives aren't collated plans or complicated flowcharts—they're short, impactful statements that are easy to memorize and communicate. There are four basic components every business objective should have:

A growth-oriented intention (improve efficiency)

One or more actions (implement monthly training sessions)

A measurement for success (20% increase)

A timeline to reach success (by end of year)

Our SaaS product's implementation team will grow to five during the next fiscal year. This will require us to submit a budget proposal by the end of the quarter and look into restructured growth tracks, new job posting templates, and revised role descriptions by the start of next fiscal year.

We will increase customer satisfaction for our mobile app product demonstrably by the end of the year by integrating a new AI chatbot feature. To measure the change in customer satisfaction, we will monitor ratings in the app store, specifically looking for decreases in rates of negative reviews by 5%-10% as well as increases in overall positive reviews by 5%-10%.

Each of our water filtration systems will achieve NSF certification ahead of the launch of our rebranding campaign. Our product team will establish a checklist of changes necessary for meeting certification requirements and communicate timelines to the marketing team.

HR will implement bi-annual performance reviews starting next year. Review timelines will be built into scheduling software, and HR will automate email reminders to managers to communicate to their teams.

Business objective template

Business objectives can be as simple as one action or as complex as a multi-year roadmap—but they should be able to fall into a clear, actionable framework.

Tips for achieving business objectives

Calling your shot to the left centerfield wall and hitting a ball over that wall are two different things—the same goes for setting an objective and actualizing it.

Start with clear, attainable goals: Objectives should position your business to reach broader growth goals, so start by establishing those.

Align decisions with objectives: Once you set objectives, they should inform other decisions. Decision-makers should think about how changes they make along the way affect their objectives' timelines and execution.

Listen to team members at all levels: Those most affected by organizational changes can be the ones with the least say in the matter. Great ideas and insights can come from any level—even if they're only tangentially related to an outcome.

What makes business objectives so useful is that they can help you build a plan with defined steps to reach obtainable growth goals. As (one more time) Yogi Berra also once said, "You've got to be very careful if you don't know where you are going, because you might not get there."

As you outline your objectives, here are some guides that can help you find KPIs and improvement opportunities:

Get productivity tips delivered straight to your inbox

We’ll email you 1-3 times per week—and never share your information.

Bryce Emley

Currently based in Albuquerque, NM, Bryce Emley holds an MFA in Creative Writing from NC State and nearly a decade of writing and editing experience. His work has been published in magazines including The Atlantic, Boston Review, Salon, and Modern Farmer and has received a regional Emmy and awards from venues including Narrative, Wesleyan University, the Edward F. Albee Foundation, and the Pablo Neruda Prize. When he isn’t writing content, poetry, or creative nonfiction, he enjoys traveling, baking, playing music, reliving his barista days in his own kitchen, camping, and being bad at carpentry.

- Small business

- Sales & business development

Related articles

Project milestones for improved project management

Project milestones for improved project...

14 data visualization examples to captivate your audience

14 data visualization examples to captivate...

61 best businesses to start with $10K or less

61 best businesses to start with $10K or...

SWOT analysis: A how-to guide and template (that won't bore you to tears)

SWOT analysis: A how-to guide and template...

Improve your productivity automatically. Use Zapier to get your apps working together.

- Product overview

- All features

- Latest feature release

- App integrations

CAPABILITIES

- project icon Project management

- Project views

- Custom fields

- Status updates

- goal icon Goals and reporting

- Reporting dashboards

- workflow icon Workflows and automation

- portfolio icon Resource management

- Capacity planning

- Time tracking

- my-task icon Admin and security

- Admin console

- asana-intelligence icon Asana AI

- list icon Personal

- premium icon Starter

- briefcase icon Advanced

- Goal management

- Organizational planning

- Campaign management

- Creative production

- Content calendars

- Marketing strategic planning

- Resource planning

- Project intake

- Product launches

- Employee onboarding

- View all uses arrow-right icon

- Project plans

- Team goals & objectives

- Team continuity

- Meeting agenda

- View all templates arrow-right icon

- Work management resources Discover best practices, watch webinars, get insights

- Customer stories See how the world's best organizations drive work innovation with Asana

- Help Center Get lots of tips, tricks, and advice to get the most from Asana

- Asana Academy Sign up for interactive courses and webinars to learn Asana

- Developers Learn more about building apps on the Asana platform

- Community programs Connect with and learn from Asana customers around the world

- Events Find out about upcoming events near you

- Partners Learn more about our partner programs

- Asana for nonprofits Get more information on our nonprofit discount program, and apply.

Featured Reads

- 22 types of business objectives to meas ...

22 types of business objectives to measure success

Clear business objectives help you achieve your mission statement and long-term company vision. These objectives can range from financial objectives to organization specific objectives. Take a look at 22 types of business objectives you can set—plus, learn when to use business objectives vs. 14 other goal frameworks.

Whether you work at a small business, a start up, or as a team lead at a larger enterprise, as a key business owner, you’re responsible for identifying the business objectives that will help your organization hit its long-term goals. Setting goals and strategic objectives is the best way to know where you’re going and how to get there.

In this article, learn about 22 different types of business objectives and how to make them achievable. Then, take a look at the 15 different types of goals you can set, depending on why you’re setting those goals.

What is a business objective?

Business objectives are the results you are aiming to achieve in order to accomplish your longer-term company vision. Think of business objectives as metrics to measure your overall business success.

Hitting your business objectives means you’re on the path towards achieving larger company goals. As such, business objectives should focus on large-scale organizational impact. Good business objectives are measurable, specific, and time-bound.

Unlock the true business value of Asana

Discover IDC's insights on how Asana helps businesses overcome tool overload, streamline decision-making, and boost productivity. Learn how Asana delivers 57% more on-time projects, 82% higher employee satisfaction, and an impressive ROI.

22 types of business objectives

Set business objectives based on factors that measure and impact your organization’s success. For example, you might set the following business objectives:

Financial business objectives

1. Profitability: A profitability-focused business objective is important if your company is relying on outside investors. Achieving—and maintaining—profitability ensures your long-term success so you can make progress towards your overall company mission.

2. Revenue: Revenue-focused business objectives help you balance your income with your costs in order to stay in business. You might set business objectives to achieve a certain annual revenue goal, or to increase revenue by a certain percentage over a period of time.

3. Costs: Costs refer to how much money you’re spending on your business. Reducing costs can help you increase revenue and achieve profitability. Business objectives related to cost can help you control production or operations cost to improve your business’s financial performance.

4. Cash flow: Cash flow refers to the money moving into and out of your business. Cash flow can be positive—when you’re making more than you’re spending—or negative—when you’re spending more than you’re making. Similar to profitability, a cash flow-oriented business objective can help set you up for long term financial success.

5. Sustainable growth: In order to grow as a business, you need to grow sustainably. Setting business objectives around sustainable growth can help you plan your financial projections, employee costs, and other financial considerations.

Customer-centric business objectives

6. Competitive positioning: A big element of your business strategy is thinking about how your product or service compares to others in the same market. By setting a business objective focused on competitive positioning, you can ensure your product or service reaches parity with what’s expected in the market, or use competitive positioning to outdo your competitors in a key area.

8. Customer satisfaction: In order to succeed as a business, you need happy customers. Focusing on a customer satisfaction-based business objective can help you better serve your customers. Depending on the business objective, this might focus on a customer advocacy program, a better help desk, or something similarly customer-facing.

9. Brand awareness: Your brand is what makes your organization stand out from the crowd. Brand awareness is an important way to understand how your customers think of your brand, and how aware they are of your distinct brand vs. your competitors. Understanding—and increasing—brand awareness is a key part of your long-term marketing strategy .

10. Sales: You’ll often find business objectives related to improving or refining the sales cycle. This could include anything from reducing customer acquisition cost (CAC), developing better lead tracking, increasing cross-selling, or something else.

11. Churn: In business, your churn rate refers to how many customers you lose over a set period of time. Reducing churn is a great way to increase your revenue and ensure your customers are satisfied with the product or service you provide.

Internal business objectives

12. Employee satisfaction and engagement: Part of your business is how your employees feel about working there, too. Increasing employee satisfaction and engagement leads to happier employees, reduced burnout , and more effective teams.

13. Employee retention: A key internal business objective is how long your employees spend at your company. Increasing tenure and reducing turnover can help you achieve more complex projects with knowledgeable employees.

14. Company growth: In order to grow your business, you also need to grow the number of people you employ. Growing your company sustainably can be difficult—which is why businesses often set company growth as a key business objective.

15. Organizational culture: Organizational culture is the ideals, values, and group norms that shape how team members interact within your company. Good culture drives employee engagement and increases retention, which is one of the key reasons so many companies set organizational culture-focused business objectives.

16. Change management: Smoothly implement large-scale organizational change with change management . Though you typically won’t see organizations set this type of business objective year after year, it can be a helpful objective to set if you have large changes on the horizon.

17. Productivity: At Asana, we don’t think of productivity as “doing the most you can,” but rather as a way to optimize your time and get your best work done. Increasing employee productivity can help your teams achieve their high-impact work more efficiently.

18. Employee effectiveness: Teams don’t just need to be efficient—they also need to know the right things to work on. The best companies aim for efficiency and effectiveness—which is where an effectiveness-based business objective comes into play. To learn more, read our article about the difference between efficiency and effectiveness .

19. Diversity and inclusion: A big part of a welcoming company culture is making sure your employees feel like they belong. Investing in diversity and inclusion programs can help your business be more welcoming to your current and potential employees.

Regulation related business objectives

20. Quality control: Implementing quality control measures as a business objective can help you ensure your product or services are at the level you want them to be. This in turn leads to better customer relationships and overall increase in revenue.

21. Compliance: If your business has any compliance needs to meet in the near future, setting those compliance requirements as a business objective will ensure you hit your targets on time.

22. Sustainability or waste reduction: Some businesses set business objectives to reduce waste or increase sustainability. While this may not directly impact your business, proving that you’re environmentally minded can help you reach specific audiences you’re targeting.

Which goal framework is right for you?

Figuring out exactly what type of goal you need to set can be tricky. Each goal framework is slightly different—and implementing the right one can help you achieve success.

The type of goal you set will depend on the business activities you’re running and the specific goals you have. If your goals have a set time frame, you may want to go with short-term objectives, whereas larger goals have their own unique frameworks.

If you’re not sure where to start, check out these 15 goal frameworks for different situations:

1. Business objectives: Set goals based on operating factors that impact your company’s long-term success.

2. Business plan : Also called a business strategy plan. Document your business’ goals and plan out how you’ll get there.

3. Vision statement : Set an organization-wide North Star.

4. Big Hairy Audacious Goals (BHAGs) : Set organization-sized stretch goals .

5. Company values : Align your team around core principles.

6. Strategic plan : Clarify your three to five year company goals during the strategic planning process.

7. Strategic goal : Set the goals you want to achieve by the end of your strategic plan.

8. Critical success factors : Clarify the high-level goals you need to achieve in order to achieve your strategic goals.

9. Strategic management : Execute against your strategic plan in order to achieve your company goals.

10. Business goals : Set predetermined targets to achieve in a set period of time.

11. Objectives and key results (OKRs) : Set and communicate annual company goals.

12. Key performance indicators (KPIs) : Set quantitative goals.

13. Project objectives : Share what you want to achieve by the end of a project.

14. Project deliverables : Identify a project’s output.

15. Project milestones : Mark specific checkpoints along a project’s timeline.

More goal setting resources

Clear goals are critical to keep your organization functioning. In addition to business objectives, check out our goal setting resource hub for tips on setting goals and achieving high-impact results. Then when you’re ready, get started with Asana for goal tracking. With Asana , you can connect your company goals to the work that supports them—all in one place.

Related resources

What's the difference between accuracy and precision?

How Asana streamlines strategic planning with work management

What is management by objectives (MBO)?

7 steps to complete a social media audit (with template)

Business Goals 101: How to Set, Track, and Achieve Your Organization’s Goals with Examples

By Kate Eby | November 7, 2022

- Share on Facebook

- Share on LinkedIn

Link copied

Learning how to set concrete, achievable business goals is critical to your organization’s success. We’ve consulted seasoned experts on how to successfully set and achieve short- and long-term business goals, with examples to help you get started.

Included on this page, you’ll find a list of the different types of business goals , the benefits and challenges of business goal-setting, and examples of short-term and long-term business goals. Plus, find expert tips and compare and contrast business goal-setting frameworks.

What Are Business Goals?

Business goals are the outcomes an organization aims to achieve. They can be broad and long term or specific and short term. Business leaders set goals in order to motivate teams, measure progress, and improve performance.

“Business goals are those that represent a company's overarching mission,” says David Bitton, Co-founder and CMO of DoorLoop . “These goals typically cover the entire business and are vast in scope. They are established so that employees may work toward a common goal. In essence, business goals specify the ‘what’ of a company's purpose and provide teams with a general course to pursue.”

For more resources and information on setting goals, try one of these free goal tracking and setting templates .

Business Goals vs. Business Objectives

Many professionals use the terms business goal and business objective interchangeably. Generally, a business goal is a broad, long-term outcome an organization works toward, while a business objective is a specific and measurable task, project, or initiative.

Think of business objectives as the steps an organization takes toward their broader, long-term goals. In some cases, a business objective might simply be a short-term goal. In most cases, business goals refer to outcomes, while business objectives refer to actionable tasks.

“Business objectives are clear and precise,” says Bitton. “When businesses set out to achieve their business goals, they do so by establishing quantifiable, simply defined, and trackable objectives. Business objectives lay out the ‘how’ in clear, doable steps that lead to the desired result.”

For more information and resources, see this article on the key differences between goals and objectives.

Common Frameworks for Writing Business Goals

Goal-setting frameworks can help you get the most out of your business goals. Common frameworks include SMART, OKR, MBO, BHAG, and KRA. Learning about these goal-setting tools can help you choose the right one for your company.

Here are the common frameworks for writing business goals with examples:

- SMART: SMART goals are specific, measurable, achievable, relevant, and time-bound. This is probably the most popular method for setting goals. Ensuring that your goals meet SMART goal criteria is a tried and true way to increase your chances of success and make progress on even your most ambitious goals. Example SMART Goal: We will increase the revenue from our online store by 5 percent in three months by increasing our sign-up discount from 25 to 30 percent.

- OKR: Another popular approach is to set OKRs, or objectives and key results. In order to use OKRs , a team or individual selects an objective they would like to work toward. Then they select key results , or standardized measurements of success or progress. Example Objective: We aim to increase the sales revenue of our online store. Example Key Result: Make $200,000 in sales revenue from the online store in June.

- MBO: MBO, or management by objectives , is a collaborative goal-setting framework and management technique. When using MBO, managers work with employees to create specific, agreed-upon objectives and develop a plan to achieve them. This framework is excellent for ensuring that everyone is aligned on their goals. Example MBO: This quarter, we aim to decrease patient waiting times by 30 percent.

- BHAG: A BHAG, or a big hairy audacious goal , is an ambitious, possibly unattainable goal. While the idea of setting a BHAG might run contrary to a lot of advice about goal-setting, a BHAG can energize the team by giving everyone a shared purpose. These are best for long-term, visionary business goals. Example BHAG: We want to be the leading digital music service provider globally by 2030.

- KRA: KRAs, or key result areas , refer to a short list of goals that an individual, department, or organization can work toward. KRAs function like a rubric for general progress and to help ensure that the team’s efforts have an optimal impact on the overall health of the business. Example KRA: Increase high-quality sales leads per sales representative.

Use the table below to compare the pros and cons of each goal-setting framework to help you decide which framework will be most useful for your business goals.

| Framework | Pros | Cons |

|---|---|---|

| SMART (specific, measurable, achievable, relevant, time-bound) | ||

| OKRs (objectives and key results) | ||

| MBOs (management by objectives) | ||

| BHAGs (big hairy audacious goals) | ||

| KRAs (key results areas) |

Types of Business Goals

A business goal is any goal that helps move an organization toward a desired result. There are many types of business goals, including process goals, development goals, innovation goals, and profitability goals.

Here are some common types of business goals:

- Growth: A growth goal is a goal relating to the size and scope of the company. A growth goal might involve increasing the number of employees, adding new verticals, opening new stores or offices, or generally expanding the impact or market share of a company.

- Process: A process goal , also called a day-to-day goal or an efficiency goal , is a goal to improve the everyday effectiveness of a team or company. A process goal might involve establishing or improving workflows or routines, delegating responsibilities, or improving team skills.

- Problem-Solving: Problem-solving goals address a specific challenge. Problem-solving goals might involve removing an inefficiency, changing policies to accommodate a new law or regulation, or reorienting after an unsuccessful project or initiative.

- Development: A development goal , also called an educational goal , is a goal to develop new skills or expertise, either for your team or for yourself. For example, development goals might include developing a new training module, learning a new coding language, or taking a continuing education class in your field.

- Innovation: An innovation goal is a goal to create new or more reliable products or services. Innovation goals might involve developing a new mobile app, redesigning an existing product, or restructuring to a new business model.

- Profitability: A profitability goal , also called a financial goal , is any goal to improve the financial prospects of a company. Profitability goals might involve increasing revenue, decreasing debt, or growing the company’s shareholder value.

- Sustainability: A s ustainability goal is a goal to either decrease your company’s negative impact on the environment or actively improve the environment through specific initiatives. For example, a sustainability goal might be to decrease a company’s carbon footprint, reduce energy use, or divest from environmentally irresponsible organizations and reinvest in sustainable ones.

- Marketing: A marketing goal , also called a brand goal , is a goal to increase a company’s influence and brand awareness in the market. A marketing goal might be to boost engagement across social media platforms or generate more higher-quality leads.

- Customer Relations: A customer relations goal is a goal to improve customer satisfaction with and trust in your product or services. A customer relations goal might be to decrease customer service wait times, improve customers’ self-reported satisfaction with your products or services, or increase customer loyalty.

- Company Culture: A company culture goal , also called a social goal , is a goal to improve the work environment of your company. A company culture goal might be to improve employee benefits; improve diversity, equity, and inclusion (DEI) across your organization; or create a greater sense of work-life balance among employees.

What Are Business Goal Examples?

Business goal examples are real or hypothetical business goal statements. A business goal example can use any goal-setting framework, such as SMART, OKR, or KRA. Teams and individuals use these examples to guide them in the goal-setting process.

For a comprehensive list of examples by industry and type, check out this collection of business goal examples .

What Are Short-Term Business Goals?

Short-term business goals are measurable objectives that can be completed within hours, days, weeks, or months. Many short-term business goals are smaller objectives that help a company make progress on a longer-term goal.

The first step in setting a short-term business goal is to clarify your long-term goals.

“My practice is to start with an aspirational vision that is the framework for my long-term goals and to compare that ‘better tomorrow’ with the realities of today,” says Morgan Roth, Chief Communication Strategy Officer at EveryLife Foundation for Rare Diseases . “Once that framework of three to five major goals is drafted and I have buy-in, I can think about how we get there. Those will be my short-term goals.”

Bitton recommends using the SMART framework for setting short-term business goals to ensure that your team has structure and that their goals are achievable. “Determine which objectives can be attained in a reasonable amount of time,” she adds. “This will help you stay motivated. Your organization may suffer if you try to squeeze years-long ambitions into a month-long project.”

Short-Term Business Goal Examples

Companies can use short-term business goals to increase profits, implement new policies or initiatives, or improve company culture. We’ve gathered some examples of short-term business goals to help you brainstorm your own goal ideas.

Here are three sample short-term business goals:

- Increase Your Market Share: When companies increase their market share, they increase the percentage of their target audience who chooses their product or service over competitors. This is a good short-term goal for companies that have long-term expansion goals. For example, a local retail business might want to draw new customers from the local community. The business sets a goal of increasing the average number of customers who enter its store from 500 per week to 600 per week within three months. It can meet this goal by launching a local advertising initiative, reducing prices, or expanding its presence on local social media groups. Small business owners can check out this comprehensive guide to learn more about setting productive goals for their small businesses.

- Reduce Paper Waste: All businesses produce waste, but company leaders can take actions to reduce or combat excessive waste. Reducing your company’s paper waste is a good short-term goal for companies that have long-term sustainability goals. For example, a large company’s corporate headquarters is currently producing an average of four pounds of paper waste per employee per day. They set a goal of decreasing this number to two pounds by the end of the current quarter. They can meet this goal by incentivizing or requiring electronic reporting and forms whenever possible.

- Increase Social Media Engagement: High social media engagement is essential for businesses that want to increase brand awareness or attract new customers. This is a good short-term goal for companies with long-term marketing or brand goals. For example, after reviewing a recent study, a natural cosmetics company learns that its target audience is 30 percent more likely to purchase products recommended to them by TikTok influencers, but the company’s social media team only posts sporadically on its TikTok. The company sets a goal of producing and posting two makeup tutorials on TikTok each week for the next three months.

What Are Long-Term Business Goals?

A l ong-term business goal is an ambitious desired outcome for your company that is broad in scope. Long-term business goals might be harder to measure or achieve. They provide a shared direction and motivation for team members.

“Long-term planning is increasingly difficult in our very complex and interconnected world,” says Roth. “Economically, politically, and culturally, we’re seeing sea changes in the way we live and work. Accordingly, it’s important to be thoughtful about long-term goal-setting, but not to the point where concerns stifle creativity and your ‘Big Ideas.’ A helpful strategy I employ is to avoid assumptions. Long-term planning should be based on what you know, not on what you assume will be true in some future state.”

Tip: You can turn most short-term goals into long-term goals by increasing their scope. For example, to turn the “increase market share” goal described above into a long-term goal, you might increase the target weekly customers from 600 to 2,000. This will likely take longer than a few months and might require expanding the store or opening new locations.

Long-Term Business Goal Examples

An organization can use long-term business goals to unify their vision, motivate workers, and prioritize short-term goals. We’ve gathered some examples of long-term business goals to guide you in setting goals for your business.

Here are three sample long-term business goals:

- Increase Total Sales: A common growth profitability goal is to increase sales. An up-and-coming software company might set a long-term goal of increasing their product sales by 75 percent over two years.

- Increase Employee Retention: Companies with high employee retention enjoy many benefits, such as decreased hiring costs, better brand reputation, and a highly skilled workforce. A large corporation with an employee retention rate of 80 percent might set a long-term goal of increasing that retention rate to 90 percent within five years.

- Develop a New Technology: Most companies in the IT sphere rely on innovation goals to stay competitive. A company might set a long-term goal of creating an entirely new AI technology within 10 years.

Challenges of Setting Business Goals

Although setting business goals has few downsides, teams can run into problems. For example, setting business goals that are too ambitious, inflexible, or not in line with the company vision can end up being counterproductive.

Here are some common challenges teams face when setting business goals:

- Having a Narrow Focus: One of the greatest benefits of setting business goals is how doing so can focus your team. That said, this can also be a drawback, as such focus on a single goal can narrow the team’s perspective and make people less able to adapt to change or recognize and seize unexpected opportunities.

- Being Overly Ambitious: It’s important to be ambitious, but some goals are simply too lofty. If a goal is impossible to hit, it can be demoralizing.

- Not Being Ambitious Enough: The opposite problem is when companies are too modest with their goal-setting. Goals should be realistic but challenging. Teams that prioritize the former while ignoring the latter will have problems with motivation and momentum.

- Facing Unexpected Obstacles: If something happens that suddenly derails progress toward a goal, it can be a huge blow to a company. Learn about project risk management to better manage uncertainty in your projects.

- Having Unclear Objectives: Goals that are vague or unquantifiable will not be as effective as clear, measurable goals. Use frameworks such as SMART goals or OKRs to make sure your goals are clear.

- Losing Motivation: Teams can lose sight of their goals over time, especially with long-term goals. Be sure to review and assess progress toward goals regularly to keep your long-term vision front of mind.

Why You Need Business Goals

Every business needs to set clear goals in order to succeed. Business goals provide direction, encourage focus, improve morale, and spur growth. We’ve gathered some common benefits of goal-setting for your business.

Here are some benefits you can expect from setting business goals:

- More Clarity: Business goals ensure that everyone is moving toward a determined end point. Companies with clear business goals have teams that agree on what is important and what everyone should be working toward.

- Increased Focus: Business goals encourage focus, which improves performance and increases productivity.

- Faster Growth: Business goals help companies expand and thrive. “Setting goals and objectives for your business will help you grow it more quickly,” says Bitton. “Your potential for growth increases as you consistently accomplish your goals and objectives.”

- Improved Morale: Everyone is happier when they are working toward a tangible goal. Companies with clear business goals have employees that are more motivated and fulfilled at work. Plus, measuring progress toward specific goals makes it easier to notice and acknowledge everyone’s successes.

- More Accountability: Having tangible goals means that everyone can see whether or not their work is effective at making progress toward those goals.

- Better Decision-Making: Business goals help teams prioritize tasks and make tough decisions. “You gain perspective on your entire business, which makes it easier for you to make smart decisions,” says Bitton. “You are forming a clear vision for the direction you want your business to go, which facilitates the efficient distribution of resources, the development of strategies, and the prioritization of tasks.”

Improve Your Goal-Setting with Real-Time Work Management in Smartsheet

Empower your people to go above and beyond with a flexible platform designed to match the needs of your team — and adapt as those needs change.

The Smartsheet platform makes it easy to plan, capture, manage, and report on work from anywhere, helping your team be more effective and get more done. Report on key metrics and get real-time visibility into work as it happens with roll-up reports, dashboards, and automated workflows built to keep your team connected and informed.

When teams have clarity into the work getting done, there’s no telling how much more they can accomplish in the same amount of time. Try Smartsheet for free, today.

Discover why over 90% of Fortune 100 companies trust Smartsheet to get work done.

- Business Essentials

- Leadership & Management

- Credential of Leadership, Impact, and Management in Business (CLIMB)

- Entrepreneurship & Innovation

- Digital Transformation

- Finance & Accounting

- Business in Society

- For Organizations

- Support Portal

- Media Coverage

- Founding Donors

- Leadership Team

- Harvard Business School →

- HBS Online →

- Business Insights →

Business Insights

Harvard Business School Online's Business Insights Blog provides the career insights you need to achieve your goals and gain confidence in your business skills.

- Career Development

- Communication

- Decision-Making

- Earning Your MBA

- Negotiation

- News & Events

- Productivity

- Staff Spotlight

- Student Profiles

- Work-Life Balance

- AI Essentials for Business

- Alternative Investments

- Business Analytics

- Business Strategy

- Business and Climate Change

- Creating Brand Value

- Design Thinking and Innovation

- Digital Marketing Strategy

- Disruptive Strategy

- Economics for Managers

- Entrepreneurship Essentials

- Financial Accounting

- Global Business

- Launching Tech Ventures

- Leadership Principles

- Leadership, Ethics, and Corporate Accountability

- Leading Change and Organizational Renewal

- Leading with Finance

- Management Essentials

- Negotiation Mastery

- Organizational Leadership

- Power and Influence for Positive Impact

- Strategy Execution

- Sustainable Business Strategy

- Sustainable Investing

- Winning with Digital Platforms

Setting Business Goals & Objectives: 4 Considerations

- 31 Oct 2023

Setting business goals and objectives is important to your company’s success. They create a roadmap to help you identify and manage risk , gain employee buy-in, boost team performance , and execute strategy . They’re also an excellent marker to measure your business’s performance.

Yet, meeting those goals can be difficult. According to an Economist study , 90 percent of senior executives from companies with annual revenues of one billion dollars or more admitted they failed to reach all their strategic goals because of poor implementation. In order to execute strategy, it’s important to first understand what’s attainable when developing organizational goals and objectives.

If you’re struggling to establish realistic benchmarks for your business, here’s an overview of what business goals and objectives are, how to set them, and what you should consider during the process.

Access your free e-book today.

What Are Business Goals and Objectives?

Business objectives dictate how your company plans to achieve its goals and address the business’s strengths, weaknesses, and opportunities. While your business goals may shift, your objectives won’t until there’s an organizational change .

Business goals describe where your company wants to end up and define your business strategy’s expected achievements.

According to the Harvard Business School Online course Strategy Execution , there are different types of strategic goals . Some may even push you and your team out of your comfort zone, yet are important to implement.

For example, David Rodriguez, global chief human resources officer at Marriott, describes in Strategy Execution the importance of stretch goals and “pushing people to not accept today's level of success as a final destination but as a starting point for what might be possible in the future.”

It’s important to strike a balance between bold and unrealistic, however. To do this, you must understand how to responsibly set your business goals and objectives.

Related: A Manager’s Guide To Successful Strategy Implementation

How to Set Business Goals and Objectives

While setting your company’s business goals and objectives might seem like a simple task, it’s important to remember that these goals shouldn’t be based solely on what you hope to achieve. There should be a correlation between your company’s key performance indicators (KPIs)—quantifiable success measures—and your business strategy to justify why the goal should, and needs to, be achieved.

This is often illustrated through a strategy map —an illustration of the cause-and-effect relationships that underpin your strategy. This valuable tool can help you identify and align your business goals and objectives.

“A strategy map gives everyone in your business a road map to understand the relationship between goals and measures and how they build on each other to create value,” says HBS Professor Robert Simons in Strategy Execution .

While this roadmap can be incredibly helpful in creating the right business goals and objectives, a balanced scorecard —a tool to help you track and assess non-financial measures—ensures they’re achievable through your current business strategy.

“Ask yourself, if I picked up a scorecard and examined the measures on that scorecard, could I infer what the business's strategy was,” Simon says. “If you've designed measures well, the answer should be yes.”

According to Strategy Execution , these measures are necessary to ensure your performance goals are achieved. When used in tandem, a balanced scorecard and strategy map can also tell you whether your goals and objectives will create value for you and your customers.

“The balanced scorecard combines the traditional financial perspective with additional perspectives that focus on customers, internal business processes, and learning and development,” Simons says.

These four perspectives are key considerations when setting your business goals and objectives. Here’s an overview of what those perspectives are and how they can help you set the right goals for your business.

4 Things to Consider When Setting Business Goals and Objectives

1. financial measures.

It’s important to ensure your plans and processes lead to desired levels of economic value. Therefore, some of your business goals and objectives should be financial.

Some examples of financial performance goals include:

- Cutting costs

- Increasing revenue

- Improving cash flow management

“Businesses set financial goals by building profit plans—one of the primary diagnostic control systems managers use to execute strategy,” Simons says in Strategy Execution . “They’re budgets drawn up for business units that have both revenues and expenses, and summarize the anticipated revenue inflows and expense outflows for a specified accounting period.”

Profit plans are essential when setting your business goals and objectives because they provide a critical link between your business strategy and economic value creation.

According to Simons, it’s important to ask three questions when profit planning:

- Does my business strategy generate enough profit to cover costs and reinvest in the business?

- Does my business generate enough cash to remain solvent through the year?

- Does my business create sufficient financial returns for investors?

By mapping out monetary value, you can weigh the cost of different strategies and how likely it is you’ll meet your company and investors’ financial expectations.

2. Customer Satisfaction

To ensure your business goals and objectives aid in your company’s long-term success, you need to think critically about your customers’ satisfaction. This is especially important in a world where customer reviews and testimonials are crucial to your organization’s success.

“Everything that's important to the business, we have a KPI and we measure it,” says Tom Siebel, founder, chairman, and CEO of C3.ai, in Strategy Execution . “And what could be more important than customer satisfaction?”

Unlike your company’s reputation, measuring customer satisfaction has a far more personal touch in identifying what customers love and how to capitalize on it through future strategic initiatives .

“We do anonymous customer satisfaction surveys every quarter to see how we're measuring up to our customer expectations,” Siebel says.

While this is one example, your customer satisfaction measures should reflect your desired market position and focus on creating additional value for your audience.

Related: 3 Effective Methods for Assessing Customer Needs

3. Internal Business Processes

Internal business processes is another perspective that should factor into your goal setting. It refers to several aspects of your business that aren’t directly affected by outside forces. Since many goals and objectives are driven by factors such as business competition and market shifts, considering internal processes can create a balanced business strategy.

“Our goals are balanced to make sure we’re holistically managing the business from a financial performance, quality assurance, innovation, and human talent perspective,” says Tom Polen, CEO and president of Becton Dickinson, in Strategy Execution .

According to Strategy Execution , internal business operations are broken down into the following processes:

- Operations management

- Customer management

While improvements to internal processes aren’t driven by economic value, these types of goals can still reap a positive return on investment.

“We end up spending much more time on internal business process goals versus financial goals,” Polen says. “Because if we take care of them, the financial goals will follow at the end of the day.”

4. Learning and Growth Opportunities

Another consideration while setting business goals and objectives is learning and growth opportunities for your team. These are designed to increase employee satisfaction and productivity.

According to Strategy Execution , learning and growth opportunities touch on three types of capital:

- Human: Your employees and the skills and knowledge required for them to meet your company’s goals

- Information: The databases, networks, and IT systems needed to support your long-term growth

- Organization: Ensuring your company’s leadership and culture provide people with purpose and clear objectives

Employee development is a common focus for learning and growth goals. Through professional development opportunities , your team will build valuable business skills and feel empowered to take more risks and innovate.

To create a culture of innovation , it’s important to ensure there’s a safe space for your team to make mistakes—and even fail.

“We ask that people learn from their mistakes,” Rodriguez says in Strategy Execution . “It's really important to us that people feel it’s safe to try new things. And all we ask is people extract their learnings and apply it to the next situation.”

Achieve Your Business Goals

Business goals aren’t all about your organization’s possible successes. It’s also about your potential failures.

“When we set goals, we like to imagine a bright future with our business succeeding,” Simons says in Strategy Execution . “But to identify your critical performance variables, you need to engage in an uncomfortable exercise and consider what can cause your strategy to fail.”

Anticipating potential failures isn’t easy. Enrolling in an online course—like HBS Online’s Strategy Execution —can immerse you in real-world case studies of past strategy successes and failures to help you better understand where these companies went wrong and how to avoid it in your business.

Do you need help setting your business goals and objectives? Explore Strategy Execution —one of our online strategy courses —and download our free strategy e-book to gain the insights to create a successful strategy.

About the Author

- Pricing Customers Get a Demo

- Platform Data Reporting Analytics Collaboration Security Integrations

- Solutions Strategic Planning Organizational Alignment Business Reporting Dashboards OKRs Project Management

- Industries Local Government Healthcare Banking & Finance Utilities & Energy Higher Education Enterprise

56 Strategic Objectives Examples to Inspire Your Company's Strategy

Ted Jackson

Ted is a Founder and Managing Partner of ClearPoint Strategy and leads the sales and marketing teams.

Boost your company's strategic alignment with these 56 examples of strategic objectives ready to implement.

Table of Contents

Strategic objectives are statements that indicate what is critical or important in your organizational strategy . In other words, they’re goals you’re trying to achieve in a certain period of time—typically 3-5 years. Your objectives link out to your measures and initiatives. Objectives are a key part of your Balanced Scorecard -- along with measures and initiatives.

This list of strategic objective examples should help you think through the various types of objectives that may work best in your organization. You’ll find all 56 of them categorized below by perspective and/or theme. Before we dive into the examples, let’s talk about how to choose the right ones for your organization. Once you have your list of objectives, you may want to consider choosing a software tool to help you track your progress.

ClearPoint Strategy offers a powerful platform designed to help you create, manage, and track your strategic objectives effectively, ensuring that your entire organization is aligned and focused. Our software offers intuitive tools that simplify the creation and management of strategic objectives, helping you monitor progress and ensure that your initiatives are on track.

Download your FREE 56 key Strategic Objective library for organizational success

Choosing the right strategic objectives.

Here’s some practical advice based on years of experience: Don’t put 56 objectives in your scorecard—that’s too many. You need to pick and choose. We recommend no more than 15 objectives maximum—you can read more about creating them here. But how do you know which objectives are right for your organization? It depends on your industry and your strategy.

Use this list of objectives to brainstorm what’s most important for your industry and your specific strategy, then build a set of objectives that best represent your organization.

Strategic Goals Based On Your Industry

What business are you in? If you’re operating in a fast-growing industry like IT, technical services, or construction, you should choose objectives that match your growth goals and include movement in a positive direction.

For example, those might include launching a new product or increasing gross revenue within the next year. If you’re in a slow-growing industry, like sugar manufacturing or coal-power production, choose company objectives that focus on protecting your assets and managing expenses, such as reducing administrative costs by a certain percentage.

Strategic Objectives For Municipalities